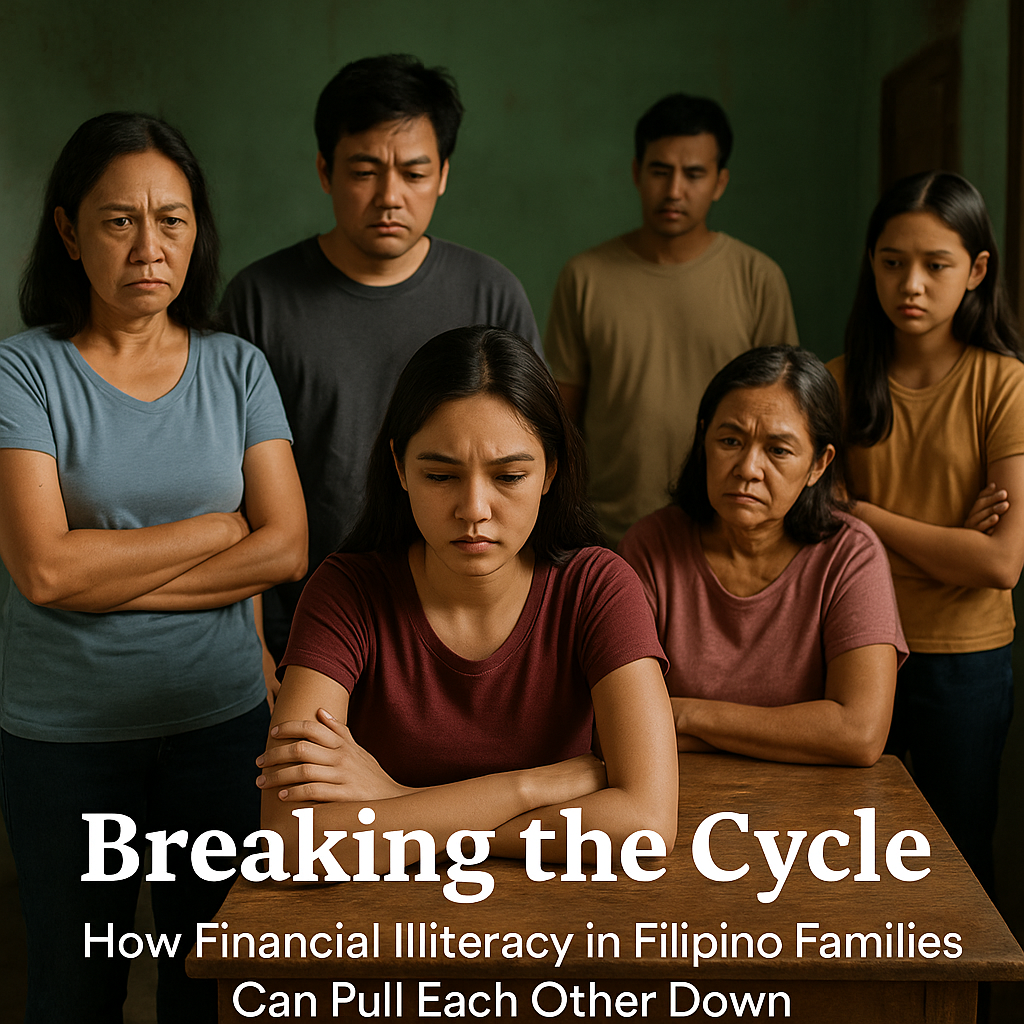

In many Filipino households, poverty isn’t just a matter of numbers — it’s a deeply rooted mindset passed down through generations. While the resilience and bayanihan (community spirit) of the Filipino people are admirable, there are also patterns of behavior that unintentionally trap families in cycles of financial struggle. One of the most overlooked causes is financial illiteracy, and the painful truth is that it often leads to family members pulling each other down without realizing it.

Imagine a young adult finally landing a decent job, earning a stable income, and dreaming of a better life. Instead of saving or investing, they are quickly burdened with the unspoken but heavy responsibility of “lifting the family.” Every paycheck is seen as a shared resource. Suddenly, cousins need tuition, parents want new appliances, and siblings expect allowance increases — all at the cost of the earner’s personal growth and financial stability.

This isn’t about selfishness; it’s about survival. But the mindset that the first to rise must carry everyone often becomes unsustainable. Worse, if the breadwinner sets boundaries or says no, they’re labeled “mayabang” (proud) or “nakalimot sa pinanggalingan” (forgot where they came from). This culture of guilt and entitlement, though unintentional, becomes a weight that prevents genuine upward mobility.

What lies at the heart of this issue is financial illiteracy — a lack of knowledge about budgeting, saving, investing, and long-term financial planning. In many poor Filipino households, conversations around money are limited to day-to-day survival. There is little discussion about how money can grow, or how financial boundaries are a form of love, not abandonment.

The result? A cycle where even the most hardworking family members burn out, financially drained before they can build anything for themselves. Opportunities are missed because of short-term thinking and a lack of education about how money works.

But here’s the good news: this cycle can be broken. It starts with financial education — not just for the one earning, but for the whole family. Teaching basic budgeting, explaining the importance of emergency funds, and shifting the mindset from “utang muna” (borrow now) to “ipon muna” (save first) can slowly reshape generational habits.

It also takes courage. The courage to say no, to create healthy financial boundaries, and to explain why. It’s not easy in a culture that values family above all else, but helping loved ones understand the bigger picture — that self-sufficiency benefits everyone — is a powerful first step.

Changing a mindset is never instant. But if one person in the family dares to lead with clarity, education, and discipline, they can influence the rest. Poverty may be inherited, but so can wisdom. And when the wisdom becomes greater than the weight, the whole family rises — not on the back of one, but together.